11% Off Travel Insurance. T&C's Apply.

10% Off* Travel Insurance! Limited time only. T&Cs apply

Not all travel insurance policies are created equal, and when it comes to protecting yourself on your next trip, knowing how to compare travel insurance properly can make all the difference.

The cheapest policy isn't always the best one, and the most expensive doesn't always mean the most comprehensive.

At 1Cover, we've spent over 20 years helping Kiwis find the right cover for their needs.

This guide walks you through everything you need to know to compare travel insurance policies with confidence; from understanding what's actually covered, to comparing prices, benefit limits, and claims processes.

Whether you're a frequent flyer, a senior traveller, a student heading overseas, a cruise-lover, an avid skier or someone with a pre-existing medical condition, this guide will help you compare travel insurance policies with confidence.

Jump to: What Should Travel Insurance Cover?, How To Compare Travel Insurance Providers, How To Compare Price, How Do Insurers Assess Pre-Existing Conditions?, How To Compare Cover Limits, How To Compare Claims Processes

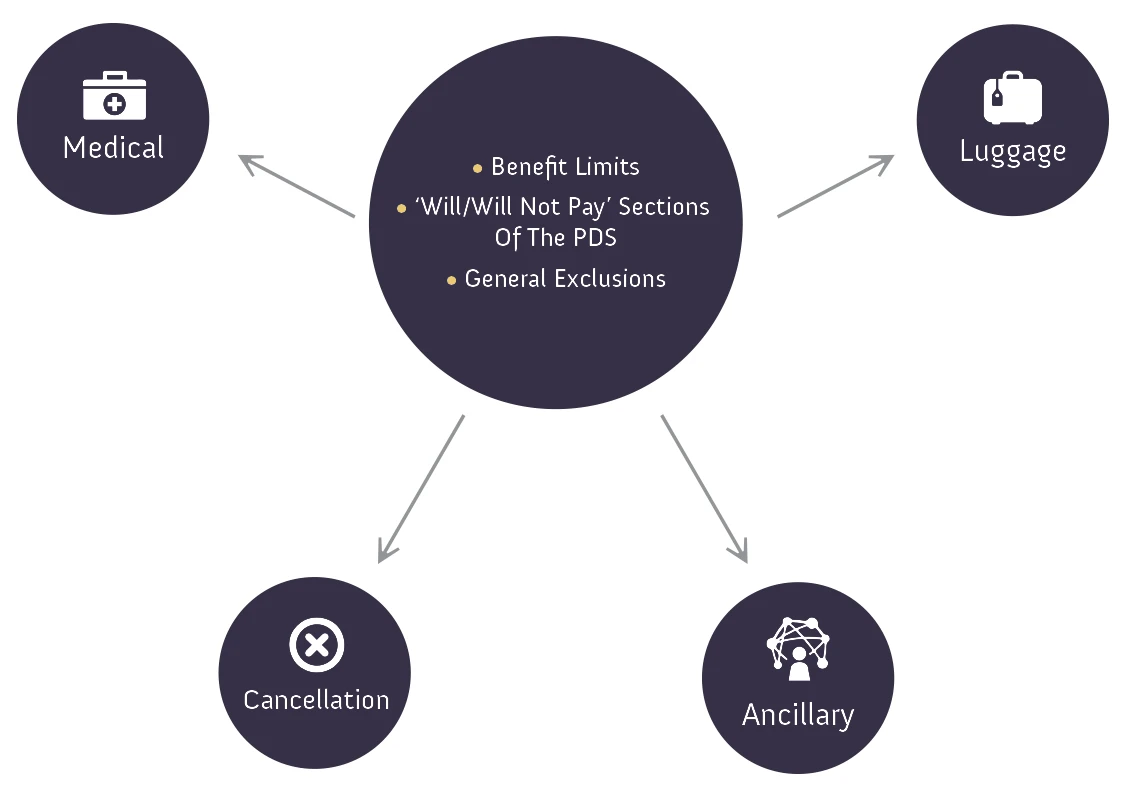

A comprehensive policy should provide cover for the following. When comparing travel insurance, be sure to check the benefit limits in relation to each component of coverage as these can change drastically between providers.

The most important aspect of your cover, after all, you can’t put a price on your health. Read more about what 1Cover can do for your medical coverage.

This will be a key consideration for any long-term trips you may have planned. Be sure to read the terms and conditions of your policy before paying any deposits for flights, accommodation or with your travel agent.

This should include not only luggage and personal effects but also delay expenses and theft of cash.

Travel insurance policies are designed to cover you for unforeseen circumstances that could occur when you’re travelling. Quickly comparing travel insurance policies can help you avoid costly emergencies abroad. Most, if not all, travel insurance policies will not cover the following instances, so keep these in mind:

Not just New Zealand laws, but be aware of local laws as well.

Be a Smart Traveller; always make sure you are up to date with the latest travel advice.

Insurers won’t cover you if you have to cancel your trip because of a natural disaster if you purchased your policy after the event was made public in the mass media. Do your research before you plan your next trip!

Leaving your things lying around is asking for someone to take them.

Be sure to use a reputable travel provider, as most insurers won't provide cover for financial collapse.

This can be a grey area, but it is a general exclusion in most, if not all, travel insurance policies.

Ignorance is not always bliss. Just because you thought something was covered doesn’t mean it will be. Always read the PDS.

Have you got an action-packed trip planned? Are you going skiing or taking part in winter sports? Generally, insurers take three different approaches to providing cover for activities:

Automatically included in your policy

Can be included at an increased premium

Excluded from cover

* Exclusions apply. See PDS for full details.

When comparing travel insurance in New Zealand, where your cover comes from can tell you a lot about the customer service, quality of cover and care you are likely to receive.

Travel insurance is the primary focus of these businesses, meaning they are specialist and experienced in the industry. They are also often the cheapest as they don’t have to pay commissions. 1Cover provides travel insurance directly to customers, and we do not pay expensive travel agent commissions, so we keep insurance premiums lower

These brands are backed by large, well-known organisations. However,travel insurance is rarely their primary focus, so they might not have the same level of expertise as travel insurance specialists like 1Cover.

Credit card travel insurance can be included in your card fees. However, be sure to check the levels of cover and benefit limits of your insurance, as these can be much lower than those from other providers. If you want to compare credit card travel insurance, check out our comprehensive guide.

Insurance provided by your travel agent may be very similar to what direct insurers provide. It is always important to know that the travel agent is acting as a middleman for another insurer, meaning you might be paying much higher premiums. Ask them what commission they get for selling Travel Insurance, and then always compare their quotes. It only takes 30 seconds to get a 1Cover quote.

On the surface, all travel insurance providers can seem the same, but if you’re going to trust them with your safety and peace of mind on your next trip, it’s important to dig a little deeper. When comparing between different providers, ask yourself the following:

Do they have a 24-hour emergency assistance service?

Are they underwritten by a company you know and trust?

Do they manage their own claims?

Do they specialise in travel insurance?

Do they have positive online customer reviews?

Just pick the cheapest one, right? Well, sort of. There are a few other things you should keep in mind when comparing travel insurance policies based on price.

When buying travel insurance, compare multiple policies for the best deal. As a general rule of thumb, the more risky your travel plans are, the higher the cost of your insurance will be. A number of variables determine the cost of your travel insurance:

The distance your destination is from New Zealand, and the cost of medical care there will affect the price of your insurance.

The longer the duration of your trip, the more your insurance will cost.

Sorry, there’s not much you can do about this.

Applying for cover for some pre-existing medical conditions may increase the cost of your policy.

Adding extras such as high-value items, ski cover, cruise cover, or rental car excess could increase the price of your policy.

Insurers assess the cost of covering your pre-existing condition differently, so be sure to raise this issue with your chosen provider.

If you don't meet the necessary criteria, you can still get travel insurance. It might just mean that:

You can obtain travel insurance, but if you want your medical condition to be covered, you'll need to pay; or

You can obtain travel insurance, but it will be mandatory to purchase coverage for your medical condition; or

Your medical condition won't be covered at all, but you can still purchase travel insurance.

Please note, that we might not be able to cover you at all, but we will tell you this during your medical assessment.

While comparing price is simple enough, comparing cover can be a little more complicated. Always remember that not all travel insurance policies are the same, and comprehensive does not necessarily mean ‘absolutely everything’ is covered. To find the right travel insurance, compare premiums and coverage limits carefully.

The key things you should look out for when comparing policies are:

The benefit limits below apply to medical claims for 1Cover comprehensive policies. These can be used as a benchmark when comparing the medical benefit limits and other benefits of other policies.

| Policy Benefits | Single-trip | Frequent Traveller | |

|---|---|---|---|

Emergency | |||

| 24/7 Emergency Assistance Service | included | included | |

Medical | |||

| Overseas Emergency Medical & Hospital Expenses | SO | unlimited | unlimited |

| Dental Expenses | O | $2,000 | $2,000 |

| Hospital Cash Allowance | SO | $10,000 | $10,000 |

| Repatriation Of Remains | O | $25,000 | $25,000 |

| Permanent Disability | O | $25,000 | $25,000 |

| Loss of Income | SO | $10,400 | $10,400 |

Benefits shown are a summary of cover only. Sub-limits may apply. Please read the Policy Wording for full terms, conditions, limits, excess payable and exclusions to determine whether our travel insurance is right for you. A Limits are per adult traveller. For accompanying dependants, the policy benefits are shared with the adult traveller. S Sub-limits apply. P Limits are per policy regardless of the number of persons the claim relates to. O There is no cover while travelling in New Zealand. |

|||

The medical benefit limits for 1Cover policies refer to the following situations:

Includes 24-hour emergency medical assistance, ambulance fees, medical evacuations, funeral arrangements, and messages to family and hospital guarantees.

Cover if you are injured or become sick overseas, including; medical, hospital, surgical and nursing.

Cover for your emergency dental treatment for the relief of sudden and acute pain to sound and natural teeth.

Cover for additional travel expenses if you cannot travel because of an injury or sickness (whilst overseas).

Cover for additional travel expenses if your travelling companion, or a relative of either of you is aged 84 or under and resides in Australia or New Zealand, dies unexpectedly, is disabled by an injury or requires hospitalisation.

Cover for additional travel and accommodation expenses to remain with your travelling companion if he or she can't continue their journey because of an injury or sickness.

An allowance of $50 per day if you are hospitalised for more than 48 continuous hours while overseas.

Funeral costs overseas, and/or repatriation costs of your remains to your home are covered.

A permanent disability benefit is payable for total loss of sight in one or both eyes or loss of use of a hand or foot (for at least 12 months, and which will continue indefinitely) within 12 months of, and because of, an injury sustained during your journey.

A weekly loss of income benefit is payable if you become disabled within 30 days of an injury you sustained during your journey, and you are still unable to work more than 30 days after returning to New Zealand.

The following benefit limits apply to luggage claims for 1Cover comprehensive policies. These can be used as a benchmark when comparing the benefit limits of other policies.

| Policy Benefit | Single | Annual | |

|---|---|---|---|

Luggage & Personal Items | |||

| Travel Documents & Transaction Cards | O | $5,000 | $5,000 |

| Theft of Cash | PO | $250 | $250 |

| Luggage & Personal Effects | AS | $15,000 | $15,000 |

| Luggage & Personal Effects Delay Expenses | ASO | $15,000 | $15,000 |

Benefits shown are a summary of cover only. Sub-limits may apply. Please read the Policy Wording for full terms, conditions, limits, excess payable and exclusions to determine whether our travel insurance is right for you. A Limits are per adult traveller. For accompanying dependants, the policy benefits are shared with the adult traveller. S Sub-limits apply. P Limits are per policy regardless of the number of persons the claim relates to. O There is no cover while travelling in New Zealand. |

|||

The luggage benefits for 1Cover policies refer to the following situations:

Cover for the replacement cost of your credit cards lost or stolen from you during your journey, and loss resulting from fraudulent use.

Cover to purchase essential items of clothing and other personal items following Luggage delayed and Personal Effects being delayed, misdirected or misplaced by your carrier for more than 12 hours.

You can choose the level of cancellation and on-trip disruption cover on 1Cover policies.

| Policy Benefit | Single-trip | |

|---|---|---|

Cancellation & Delay | ||

| Pre-Departure Cancellation Fees & Lost Deposits | PS | chosen limit |

| Pre-Departure Amendments to Journey | A | $2,000 |

On-trip Disruption | ||

| On-trip Cancellation Fees & Lost Deposits | PS | chosen limit |

| Additional Accommodation & Travel Expenses — Family Emergency — Emergency Companion Cover | AS | $50,000 |

| Travel Delay Expenses | S | $2,000 |

| Special Event Transport Expenses | O | $2,000 |

Benefits shown are a summary of cover only. Sub-limits may apply. Please read the Policy Wording for full terms, conditions, limits, excess payable and exclusions to determine whether our travel insurance is right for you. A Limits are per adult traveller. For accompanying dependants, the policy benefits are shared with the adult traveller. S Sub-limits apply. P Limits are per policy regardless of the number of persons the claim relates to. O There is no cover while travelling in New Zealand. |

||

Cancellation benefits for 1Cover policies refer to the following situations:

Cover for cancellation fees and lost deposits for pre-paid travel arrangements due to unforeseen circumstances neither expected nor intended by you, and which are outside your control, such as; sickness, injuries, strikes, collisions, retrenchment and natural disasters.

Cover for additional travel expenses following transport delays to reach events such as; a wedding, funeral, conference, sporting event and pre-paid travel/tour arrangements.

The following benefit limits apply to ancillary claims for 1Cover comprehensive policies. These can be used as a benchmark when comparing the benefit limits of other policies.

| Policy Benefit | Single-trip | Frequent Traveller | |

|---|---|---|---|

Other | |||

| Personal Liability | P | $5 million | $5 million |

| Domestic Pets | S | $500 | $500 |

| Domestic Services | SO | $500 | $500 |

Benefits shown are a summary of cover only. Sub-limits may apply. Please read the Policy Wording for full terms, conditions, limits, excess payable and exclusions to determine whether our travel insurance is right for you. A Limits are per adult traveller. For accompanying dependants, the policy benefits are shared with the adult traveller. S Sub-limits apply. P Limits are per policy regardless of the number of persons the claim relates to. O There is no cover while travelling in New Zealand. |

|||

Ancillary benefits for 1Cover policies refer to the following situations:

Cover for legal liability including legal expenses for bodily injuries or damage to property of other persons as a result of a claim made against you.

Cover for additional boarding kennel or cattery fees resulting from your delayed return home, also veterinary fees if your pet is injured while you are away.

Cover for housekeeping services following injury/disablement continuing upon your return home.

Cover for the excess payable on your rental vehicle's motor vehicle insurance resulting from the rental vehicle being; Stolen, Crashed or Damaged and/or cost of returning the rental vehicle due to you being unfit to do so.

When comparing travel insurance providers, the proof is in the pudding. When you go to make a claim, you want to know that you’re going to be looked after properly. But how will you know before purchasing a policy? While comparing travel insurance in New Zealand, use the checklist below to find out more about how your chosen provider assesses claims.

Check online to find customer reviews about your provider, paying attention to reviews that have verified claims.

Does your provider manage their own claims or outsource this to another business?

How long does it take your provider to pay claims? You can usually find this in the product disclosure statement.

Pay special attention to the general exclusions in the PDS.

Make sure your travel insurance provider is underwritten by a reputable underwriter.

![]()

Find out all you need to know to stay safe and travel happy in the USA in our USA Survival Guide .

![]()

Are you going skiing or taking part in winter sports like snowboarding or heli-skiing. Then make sure you have Ski Travel insurance

![]()

Stay safe and travel happy on your Bali holiday with this ultimate

Bali Survival Guide.

![]()

This guide will show you how to find the right cover, at the right price, no matter where you’re going.

If you have any other questions or queries, please send us a message via our Contact Us page.

If you are experiencing an emergency, please use the details on our Emergency Assistance page.

Dates

Dates

Age

Age

Extra Coverage for Skiing, Cruising, Rental Car Excess & High Value items

Extra Coverage for Skiing, Cruising, Rental Car Excess & High Value items

NZ

NZ AU

AU